When disaster strikes a home, restoration crews need more than tools and trucks—they need clarity on how the homeowners insurance dollars are divided. That’s where the three insurance “buckets” come in.

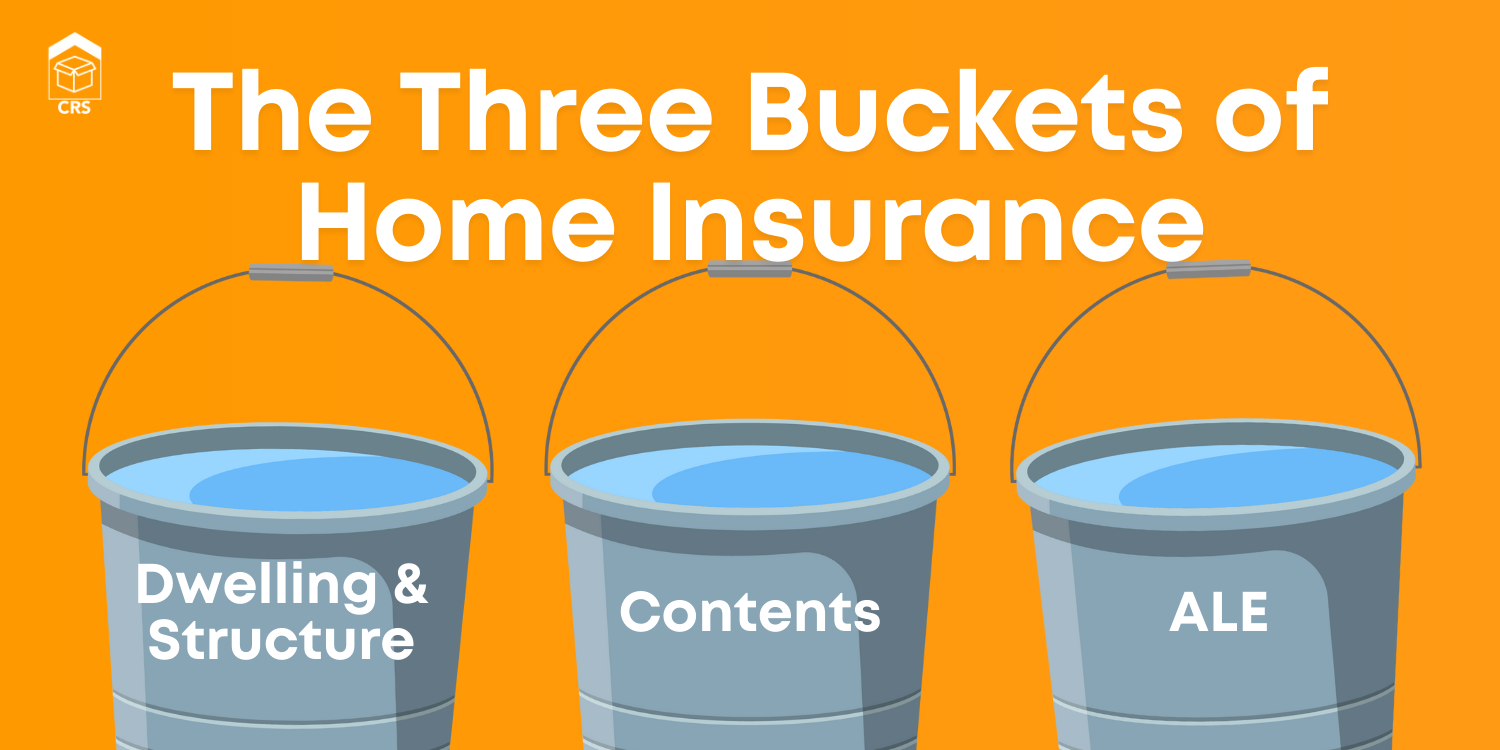

A homeowner’s policy typically splits coverage into three buckets:

- the dwelling (structure) bucket

- the personal contents bucket

- the Additional Living Expenses (ALE) bucket.

Each of these buckets operates independently, with its own set of limits, rules, and intended use. That separation is critical. You can’t pull funds from the contents bucket to pay for structural rebuilds, and ALE dollars won’t be approved to replace flooring or drywall. Insurers treat these buckets as siloed pools of money—once one runs out, you can’t dip into another to cover the gap.

For restoration contractors, this means two things:

- Accurate scoping and estimating matter more than ever. Knowing which bucket a cost falls under helps avoid denied claims and keeps projects moving forward.

- Client education is key. Homeowners often assume their coverage is one large pot, but explaining the three-bucket system early helps manage expectations about what will and won’t be covered.

By understanding how these buckets work, and where their boundaries lie, you can plan jobs with confidence, prevent costly surprises, and position yourself as a trusted advisor throughout the restoration process.

What Is Personal Property Coverage?

Personal property coverage protects the items inside a home rather than the structure itself. Think of it as everything that would fall out if you turned the house upside down and shook it. This includes:

If these items are damaged or destroyed by a covered event (such as fire, water damage, or theft), this coverage helps pay to repair or replace them.

For restoration contractors, it’s important to understand that personal property (contents) is separate from structural restoration. Each has its own scope, documentation, and insurance process.

Understanding Homeowners Insurance Coverage (Without the Confusion)

One of the most misunderstood parts of homeowners insurance is how coverage amounts are divided. Many people assume that if their policy is for $300,000, that’s the total amount available for everything — the house, the contents, and any other losses. But that’s not quite how it works.

In reality, that $300,000 figure typically refers to the cost to rebuild the home itself — known as Coverage A (Dwelling). It’s the maximum amount the insurer would pay to reconstruct a house if it were completely destroyed. This includes the structure and anything permanently attached to it, like walls, roof, foundation, and built-in appliances.

But a policy also includes other buckets of coverage, each designed to protect different parts of your property and lifestyle. These buckets are usually calculated as percentages of the dwelling coverage:

- Contents (Coverage C): Covers belongings such as furniture, electronics, clothing, etc. Often around 50% of the dwelling amount, so in a $300,000 policy, you might have $150,000 for personal property.

- Other Structures (Coverage B): Covers detached buildings like garages or sheds, usually around 10%.

- Loss of Use (Coverage D): Helps pay for temporary housing and living expenses if your home becomes uninhabitable, often around 20%.

These percentages aren’t fixed as they can vary by insurer and policy type. But the key takeaway is this:

The main policy amount is for rebuilding the home. Everything else, from contents, detached structures, to living expenses, is covered in separate buckets based on a percentage of the policy amount.

The Buckets of Home Insurance

Coverage A/B – Dwelling and Other Structures

Coverage A is the policy’s structural bucket: it covers the house itself and any attached structures (walls, roof, foundation, built-in appliances, etc.). This is usually the largest limit on the policy and covers up to the full policy limit. For example, if a house insured for $300,000 burns down, Coverage A can provide up to $300k to rebuild it – but only to rebuild the structure. Detached structures like garages, sheds or fences fall under Coverage B (Other Structures), which is commonly a small percentage of A like 10%.

- What it pays: Repair or replacement of the building’s frame, walls, roof, floors, plumbing, electrical, etc., up to the policy limit for Coverage A.

- Key point: The Dwelling bucket cannot be used to cover personal belongings or living expenses. It’s only for the physical structure (plus any attached fixtures).

If a contractor mistakenly thinks that leftover contents money can be used to patch up the structure, correct them: policies are not like a mutual fund. Each bucket has its own cap. You need enough Coverage A to do the rebuild, and if that limit is exceeded you may need a supplemental policy (e.g. builder’s risk) rather than shifting funds from Contents.

Coverage C – Personal Property (Contents)

Coverage C covers the homeowner’s personal belongings inside the home: furniture, electronics, clothing, kitchenware, tools, etc. Think of everything that would fall out if you flipped the house upside down. The dollar limit for Contents is usually set as a percentage of the dwelling (Coverage A) limit. A common default is 50% of Coverage A, although some insurers allow 70% or higher on request. For instance, on a $300,000 dwelling limit, contents might be set at $150,000. Under this coverage, the insured can claim up to that limit for repairing or replacing their belongings (often subject to depreciation rules and special sub-limits for jewelry, art, etc.).

- What it pays: Repair, cleaning or replacement of personal items in the home, up to the Contents limit. (For example, a ruined sofa or appliance.) Coverage C usually pays Actual Cash Value (depreciated) unless replacement-cost coverage is specifically purchased.

- Key point: This bucket only covers things, not the building. Even if the contents claim is far below its limit, you cannot use the leftover to rebuild a wall or roof. The limits don’t “flow” between buckets.

Common misconception:

“Work on contents takes away from the budget of structure work.”

False

Each bucket has its own maximum. If you use all your Structure money and still have personal items left, you can’t dip into the Contents bucket for more wall repairs. Likewise, saving money on structure doesn’t increase what you can pay out for furniture.

Coverage D – Loss of Use / Additional Living Expenses (ALE)

Coverage D – often called Loss of Use or Additional Living Expenses (ALE) – kicks in when the home is uninhabitable due to a covered loss. It reimburses the extra costs of living that a homeowner incurs because they’re displaced. This can include hotel or rental housing, meals (if home cooking isn’t possible), storage of personal property, transportation, and even pet boarding, up to a reasonable standard.

- Typical expenses: commonly covers hotel rent, alternate lodging, restaurant meals (only if the kitchen isn’t usable), additional utility costs, furniture rental, etc.

- Policy limit: ALE limits vary, but a common rule of thumb is 10–20% of the dwelling coverage. So if the house is insured for $300k, ALE might cap at $30k–$60k.

- Duration: Importantly, ALE pays until the home is repaired or a maximum time/money is reached. In practice, this means ALE is tied to the restoration timeline – once the house is reasonably livable (or the ALE funds run out), payments stop.

For restoration contractors, ALE matters because it affects scheduling. With ALE in place, a homeowner can stay in a hotel or rental while work proceeds. That usually reduces pressure to rush the job dangerously – you have a bit more freedom to do quality repairs if the family isn’t physically in the house. On the flip side, ALE is not unlimited: once the policy’s ALE coverage is exhausted, the homeowner will want to move back home ASAP. A savvy contractor coordinates work phases (demolition, repairs, rebuild) with the ALE clock.

Examples of ALE-covered expenses:

- Hotel or short-term rental payments (within reason, comparable to homeowner’s usual spend)

- Extra food costs (e.g. eating out if there’s no kitchen)

- Storage fees for furniture and belongings while house is gutted

- Pet lodging or childcare if needed during displacement

Example of Coverage Breakdown for a $300k Policy

Imagine this: A family’s home in Naperville, Illinois, valued at $300,000, suffers a devastating fire. While the flames are contained quickly, smoke and soot permeate every room, damaging the structure and all personal belongings. Thankfully, their homeowners insurance policy steps in to help — and here’s how each coverage pocket works:

| Coverage Type | % of Dwelling Value | Value | What it Covers |

|---|---|---|---|

| Dwelling/Structure | 100% | $300,000 | Structure repairs/rebuild |

| Contents | 50% | $150,000 | Personal belongings |

| Additional Living Expenses | 20% | $60,000 | Temp housing & living |

Working with Content Recovery Specialists

Since clearing out and restoring contents is a labor-intensive task, many restoration firms partner with content-specialist teams. Content Recovery Specialists (CRS) assess, pack out, clean, and inventory personal and commerical property. After a site has been damaged by a disaster, a CRS crew shows up, catalogs the damaged contents, and carefully packs and transports them for cleaning and storage. This frees your restoration team to focus on fixing the building.

“We partner with restoration contractors to handle the contents side of the job. This allows your team to focus on mitigation and rebuilds.”

Specialized content crews understand insurance paperwork for personal property, use digital tracking (barcodes, photos) to maintain chain-of-custody, and know how to maximize the contents coverage. In effect, they act as an extension of the homeowner’s claim team for the C bucket.

Given that content coverage is typically only a fraction of the dwelling limit, it’s critical to document everything. Work with the homeowner’s adjuster and/or public adjuster to inventory items. But remember: even a thorough contents claim can’t contribute to the structure repairs. If your demo and rebuild crew needs more space, content pack-out must be budgeted from the contents bucket.

Key Takeaways for Restoration Contractors

Separate Buckets

Remember the classic insurance metaphor: three jars of money. The “Dwelling” jar is for the building, the “Contents” jar is for personal property, and the “ALE” jar is for living costs. You can’t use pennies from one jar to cover another.

Know the Limits

Policies often set Contents at a percentage of Dwelling (commonly ~50%) and ALE around 10–20%. Before bidding work, review the adjuster’s breakdown of coverage. If the homeowner’s contents limit is nearly exhausted, don’t count on it to fund any additional tasks.

Plan the Pack-Out

First priority at a loss site is usually removing undamaged contents to clear the work area. Using professional content packout and restoration pros such as Content Recovery Specialists can speed this up. These teams will inventory and pack out belongings under the contents bucket, letting your crew handle just the structure. This also minimizes liability – handling grandma’s china is their specialty, not yours!

Factor in ALE

If the home is unlivable, ALE means the homeowner won’t be on-site, which is good for safety and pace. But monitor how long ALE will cover them. If repairs drag on past ALE coverage, the homeowner may push to finish quickly. Aim to complete critical restoration before ALE limits are hit.

Conclusion

One of the most important things restoration contractors can understand about homeowner policies is that Coverage A and Coverage C are separate buckets with separate limits. If a policy has a $300,000 limit for the structure (Coverage A), that full amount is available for rebuilding the home — and it’s not reduced by claims made under Coverage C for contents.

This distinction matters on the job site. If your team is handling structural repairs, you’re working within the Coverage A bucket. If a contents vendor is cleaning or replacing personal property, they’re pulling from Coverage C. These buckets don’t overlap, and they don’t eat into each other’s funds.

This distinction matters on the job site. If your team is handling structural repairs, you’re working within the Coverage A bucket. If a contents vendor is cleaning or replacing personal property, they’re pulling from Coverage C. These buckets don’t overlap, and they don’t eat into each other’s funds.